A home equity loan may be just what you need to pay for a new nursery.See more pictures of investing.

Photo courtesy stock.xchng

Imagine that you and your spouse have a baby on the way. You weren’t planning to start a family quite this soon and your home reflects that. The two bedroom one bath bungalow seemed like a perfect starter home for two people, but now it feels too small to include a third. You love this house, so you want to make it work. The lot’s big enough to add on an extra room - the nursery. You can just knock out the back bedroom wall and go from there. Or, maybe you could enlarge the kitchen while you’re at it, tack on a half bath and the nursery. That would be great. But where will you get the money to pay for the renovation?

In this article we’ll look at what it means to borrow against the equity of your home, what the various types of home equity loans are, and when it may be the right time to get one.

Advertisement

In the next section we will take a look at some of the basics.

Trying to figure out how to cover the finances of a bathroom remodel?A second mortgage might be your answer.

Photo courtesy stock.xchng

There are a few different types of loans that allow you to use equity in your house as collateral. One type, the more traditional of the two, is known as a home equity loan or second mortgage. When you take out a second mortgage on your home, you are borrowing one lump sum of money from the bank. You will be required to pay back the loan over a fixed period of time at a designated interest rate. For a project like a remodel or renovation, where you've gotten an estimate from the contractor and you know what you need, a second mortgage is a good idea.

Now that you understand the basics, let’s take a closer look at equity.

Advertisement

About Equity

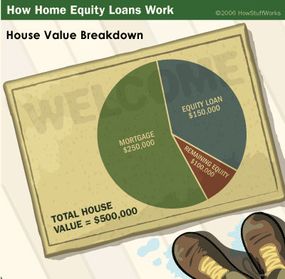

As we mentioned earlier, borrowers have several options when it comes to borrowing against the equity of their home -- a home equity loan (also commonly called a second mortgage), a home equity credit line (also called a HELOC) and a reverse mortgage. A home equity loan or second mortgage is based off of equity, or the amount of value you have in your house. Because homes generally appreciate in value over time, equity is calculated by taking the difference between the current worth of your home and how much you owe on your initial mortgage. Say you bought your house for $350,000 and you have paid off $175,000 of a $300,000 mortgage. A recent appraisal puts your home’s value at $500,000. You would calculate your current equity in your house like this:

$500,000 - $125,000 = $375,000

The $125,000 number is the amount of money yet to be paid on your mortgage. And because your house has appreciated in value -- somewhat like a stock or a valuable antique -- so has your equity in your home increased. In many cases, you may be able to use this investment to borrow against your equity in order to get another loan. And just like with your first mortgage, your house serves as the collateral that guarantees your loan to the bank. If you can’t pay off your second mortgage, you may be forced to sell your home, or the bank might seize it.

Frequently, the length of a second mortgage is shorter than the first, though they can last anywhere from five to 30 years. Still, second mortgages are generally intended to be for smaller amounts than the first, for consolidating debts, financing an addition to a home or helping to pay for a child’s college tuition. But in some cases, homeowners simply wish to take advantage of a good investment by borrowing against the rising equity of their home and thereby gaining some financial flexibility.

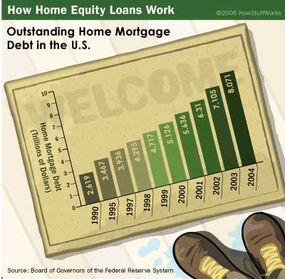

As home ownership has grown in the United States, so has mortgage debt.

Advertisement

Home Equity Loans and Reverse Mortgages

A home equity line of credit can help you pay for your kids' college tuitions.

Photo courtesy stock.xchng

A home equity loan is most useful when you need a specific amount of money for a project or investment. As we’ve established, a home equity loan involves borrowing against the equity in your house. The loan comes in a fixed amount that is repayable over a set period of time, which is why this type of loan is commonly referred to as a second mortgage. The payment schedule is usually designed around equal payments that will eventually pay off the entire loan.

Like with other types of equity plans, the interest on a home equity loan may be tax deductible up to $100,000.

Advertisement

As with a home equity loan, the borrower’s home serves as the collateral in a Home Equity Credit Line (HELOC). In a basic sense, a HELOC works like a kind of credit card. The lender examines various factors like the borrower’s income, credit history, expenses and other debts and sets the credit limit at a percentage of the home’s equity.

There is a fixed time frame applied to a HELOC, but it works slightly differently than with a home equity loan. The first time frame -- say, five years -- is the period during which the borrower can draw money using special checks, electronic transfers or even a special credit card. Different plans have different rules, but in some cases a minimum amount has to be withdrawn each time. Like a credit card, the borrower has a limit on how much money is at his or her disposal. If the borrower reaches the pre-established limit, he or she cannot borrow any more money without paying off some of the outstanding debt.

The second time frame comes at the end of the borrowing period. Some plans have an option for renewing the credit line while others require a repayment of the debt -- usually over another fixed time period. In other cases, the outstanding debt can be “rolled” into a traditional loan at the end of the drawing period.

Because the terms of home equity credit lines vary, it’s important to find one that fits your specific needs. When choosing one of these plans, consider the annual percentage rate (APR) and other costs of the plan. Like many other types of loans, a home equity plan can come with many fees attached, though some lenders may dispense with some, or even all, of the charges. In any case, these charges often include an application fee, property appraisal, initial charges such as points (which go against your credit limit), attorney’s fees, title search, mortgage preparation and filing fees, property and title insurance, taxes, membership or maintenance fees and even transaction fees when drawing on the line of credit.

The structure of the drawing and repayment periods should be considered carefully. Is the repayment period too short? Will you be able to make payments against the interest during your drawing period? These are only some of the questions to ask when considering a home equity line of credit. Also, if you are concerned that the ability to draw on a line of credit almost at will offers too much flexibility or will tempt you to spend excessively, then this is probably not the type of loan for you. But if you need money in installments -- perhaps for paying a contractor for more than one project or paying tuition, a home equity line of credit can be a very good choice.

Reverse Mortgages

A reverse mortgage can seem like a contradiction in terms. It’s money that the bank pays you that you might not have to repay for the rest of your life. You don’t even have to have an income to be eligible.

There are, of course, conditions attached to a reverse mortgage. First, you have to be at least 62 years of age and live in the home applying for the reverse mortgage for at least 50 percent of the year. You also have to own your home. In some cases, if you have a relatively small amount remaining on your home mortgage, you can get a cash advance from the reverse mortgage to pay off the rest of the debt on your house.

But the idea of a loan that you never have to repay can be misleading. If you sell your reverse mortgaged home or permanently move out, you have to repay the loan. If you do stay in the home and maintain the reverse mortgage until you pass away, the mortgage is designed to be paid off with the value of the home. But if your heirs wish to keep the house, they will have to pay off the loan. Otherwise, it will likely become property of the lender, or if the home is worth more than the loan balance, your heirs may sell the home, repay the loan and retain the difference.

Unlike a traditional or “forward” mortgage, a reverse mortgage involves rising debt and falling equity. Your debt increases as your equity decreases.

A reverse mortgage could help you buy that boat you've been eyeing since you retired, but it's important to know that eventually someone will have to repay the loan.

Photo courtesy stock.xchng

Among the different types of reverse mortgages, a Home Equity Conversion Mortgage (HECM) is the only reverse mortgage that’s federally insured. The HECM program limits loan costs and tells the lender how much they can lend you. This mortgage can be cheaper than other reverse mortgages. Usually only reverse mortgages offered by state and local governments are cheaper than an HECM, but those often must be used for a particular purpose and are mostly available to those in lower income brackets. If you’re interested in how much you can receive through an HECM or a Home Keeper Mortgage from Fannie Mae, try this mortgage calculator.

Consider This!

Before getting a reverse mortgage, it’s important to consider whether it’s worth it. Many people, if faced with debt or significant expenses in their retirement years, don’t want to sell their homes, whether for sentimental reasons or because of the work associated with moving. But it’s good to calculate how much money you can get from selling your home and compare that to how much it would cost to buy and maintain (or to rent) a new home. In the end, it may be to your financial benefit (and help your heirs later on) to move to a smaller or more easily maintained home rather than taking on a reverse mortgage. The extra capital you get from selling your home and moving to a smaller place could be used to supplement your retirement income and rule out the need for a reverse mortgage. For more information about housing options, try the AARP. There may be more choices than you think.

Advertisement

Read the Fine Print

Taking out a home equity loan puts your home on the line. Make sure that you can afford the terms and conditions of the loan agreement.

Photo courtesy stock.xchng

To protect consumers from entering into unfair loan agreements, the United States Congress passed the Consumer Credit Protection Act, also known as the Truth in Lending Act, in 1968. According to the act’s provisions, a lender must disclose important terms and costs of home equity plans, APR, payment terms, information about variable rates and any other miscellaneous charges. The act also allows three business days from the time an account is opened for the consumer to cancel the agreement. In case the borrower does decide to cancel the loan, he or she must inform the creditor in writing, and the creditor then has to cancel their security interest in the borrower’s home and return all application and loan fees.

The Consumer Credit Protection Act is especially important when considering that some people seeking second mortgages may be in difficult, or even desperate, financial conditions. Because of that, unscrupulous lenders may try to take advantage and offer them terms which they cannot afford or secretly change aspects of a loan agreement.

Advertisement

If the three-business day cancellation period passes and you decide that you have somehow been taken advantage of, report your lender to the Federal Trade Commission. You can also contact consumer protection agencies, housing counseling agencies or your state bar association for referral to a lawyer.

Differences and Similarities

One advantage of a home equity loan is its fixed interest rate -- you know how much you’re going to be charged each month. A home equity line of credit generally has a variable interest rate based on a publicly available index. While a variable interest rate means more uncertainty regarding how much you’re going to be paying in interest, it also offers some flexibility in that you’ll usually have the option of paying interest only, or paying interest and some of the principal.

The indexes that determine interest rates are the prime rate found in newspapers or the U.S. Treasury Bill (“T-Bill”) rate. A variable interest rate will change as these interest rates change, but a variable rate plan must also have a cap on how high the rate can go during the term of the plan. Some also have limits on how much the interest rate can decrease. These rates change when the Fed raises or lowers interest rates. Keep in mind that many lenders add a margin to their interest rates, which is usually measured in points. For example, if the prime rate is 4.5 percent but your lender’s rate includes a one-point margin, then your interest rate will be 5.5 percent.

Some lenders allow you to convert from a variable rate to a fixed-rate during a home equity plan, or to convert some or all of your debt to a fixed-term installment plan. Other lenders may not allow you to withdraw money when your interest rate reaches the pre-established cap.

Advertisement

Repayment and Some Tips

The repayment process for a home equity loan or a home equity line of credit is dependent on the terms of the plan. Some equity plans only require you to pay interest during the loan, leaving the entire principal to be paid once the loan is due.

If your plan’s payment schedule leaves a remaining balance at the end of the plan, be prepared to make a balloon payment. A balloon payment can be done with money on hand, by refinancing the loan or by taking out a loan from another lender. Not being able to pay a balloon payment means that you could lose your home.

Advertisement

Usually your payments options are flexible, allowing you to pay more than the minimum payment. Because of this flexibility, many home equity borrowers make regular payments to the principal in order to avoid being stuck with an outstanding balance when the loan is due. If for some reason you decide to sell your home before the end of your plan, you will probably have to repay your equity loan.

Advice for Equity Plans

Before you decide to get a home equity loan or HELOC, ask yourself if you can afford to take on more debt. Is your employment situation stable, and if so, will you be able to eventually pay back the loan? If you’re dealing with money problems, talking with a credit counseling agency can be very helpful. If the problem is in paying your mortgage, you can get a listing of approved housing counseling agencies from the Department of Housing and Urban Development. In general, it’s best to get a home equity loan only when you have a specific use in mind for it. While a home equity line of credit offers more flexibility than a home equity loan (second mortgage), using it like just another credit card can get you in trouble down the road.

Once you’ve decided you need a home equity loan, it’s important to shop around. Make sure the lenders you talk to are reputable. Predatory lenders prey on the elderly, attempting to trick them into accepting unmanageable loans, or on people with low income or credit problems. Ask friends and relatives about the banks they have dealt with, and research the lenders you’re working with to make sure they’re dealing in good faith.

With so many fees associated with a loan and things like variable interest rates, it can be hard to determine exactly what makes one lender better than another. Try using this worksheet from the FDIC for comparing different loan offers. It will give you some good questions to ask and will allow you to keep the information about each lender organized.

Don’t hesitate to negotiate with your prospective lenders. Think of it like shopping for a car. Let them know you’re shopping around, and ask them to lower the various rates, fees and points. Make them beat the terms of another lender.

Once you select a lender, get a “good faith estimate” of all charges. By law, the lender must send you an estimate within three days of your application. Study the forms you receive, and most of all, ask questions! One or two weeks before closing, ask the lender if the terms have changed from what was in the good faith estimate.

If you know someone with loan experience, such as an accountant or tax attorney, ask them to look over the estimate, loan papers and contract. Again, make sure to ask any questions you may have. Don’t be rushed into signing a contract if you’re unsure of something or if some language in the agreement is unclear. Don’t sign forms that have blank fields. If your lender tells you they are supposed to be blank, draw a line through the field and initial it.

Most of all, don’t get a loan for more money than you need or for terms you can’t afford. Even if the lender promises you that the terms are favorable, taking on a high loan-to-value ratio can make repaying the loan difficult and jeopardize your home ownership. The loan-to-value ratio is the ratio of what you owe on your house to its overall value. Generally, lenders try to keep your loan-to-value ratio below 80 percent. For example, if you owe $250,000 on a $500,000 house, you already have a loan-to-value ratio of 0.50 or 50 percent. For a second mortgage, a lender likely won’t offer you more than $150,000, which would put you at $400,000 in total loans -- or a loan-to-value ratio of 80 percent ($400,000 divided by $500,000).

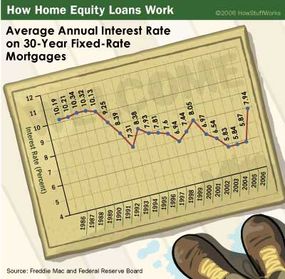

It's important to avoid getting tied up with too much mortgage debt.

Try to have a loan-to-value ratio under 80 percent.

Some lenders will go over 80 percent or even offer you a loan for more than your home is worth. Try to avoid those loans as they will likely carry higher interest rates, require mortgage insurance and be more difficult to pay off if you’re forced to sell your home.

For more information about home equity loans and related topics, check out the links on the following page.

Advertisement

Home Equity Loans FAQ

How does a home equity loan work?

A home equity loan allows you to borrow against the equity of your home or take a "second mortgage". Much like a regular mortgage, you borrow one lump sum of money from the lender, which you're required to pay back over a fixed period of time at a specific interest rate.

How much can you borrow on a home equity loan?

Generally, lenders will allow you to borrow up to around 80 to 90% percent of your available equity (the amount of value you have in your house) depending on the lender, your credit score, and income. For example, let's say you bought your house for $350,000 and you have paid off $175,000 of a $300,000 mortgage, meaning you still have $125,000 to pay back. A recent appraisal values your house at $500,000 now. You would calculate your current equity in your house like this: $500,000 - $125,000 = $375,000. Your specific lender will have a percentage of that $375,000 that they'll allow you to borrow.

Is it better to get a home equity loan or line of credit?

A home equity loan may be best if you prefer fixed monthly repayments and know exactly how much you need for a goal or home improvement project. A home equity line of credit may be a better fit for financial needs that are spread over time, or if you want flexible access — after all, it functions kind of like a credit card. The terms of these credit lines vary, so it’s important to find one that fits your specific needs.

Can you use a home equity loan on anything?

You can legally use a home equity loan to pay for anything though most people use them for large expenses such as home renovations, medical expenses, or education costs.

What is the average interest rate on a home equity loan?

The rate you'll be offered will depend largely on your personal circumstances, and what the going interest rate is at the time.

"A "Rising Debt" Loan." AARP. http://www.aarp.org/money/revmort/revmort_basics/ a2003-03-31-risingdebt.html

"A New Kind of Loan: In Reverse." AARP. http://www.aarp.org/money/revmort/revmort_basics/a2003-03-21-newloan.html

"About Reverse Mortgages for Seniors (HECM)." 7/14/2006. U.S. Department of Housing and Urban Development. http://www.hud.gov/offices/hsg/sfh/hecm/hecmabou.cfm

"FDIC: Putting Your Home on the Line is a Risky Business." 10/24/2003. Federal Deposit Insurance Corporation. http://www.fdic.gov/consumers/consumer/predatorylending/index.html

"Another Option: Home Equity Loans." Motley Fool. http://www.fool.com/homecenter/refinance/refinance07.htm

"Borrowing Against Your Home." Motley Fool. http://www.fool.com/homecenter/refinance/refinance02.htm